|

The Married Person Qualified Terminable Interest Property (QTIP) RLT provides the same benefits as the Single Person Basic Trust and a few additional features.

|

|

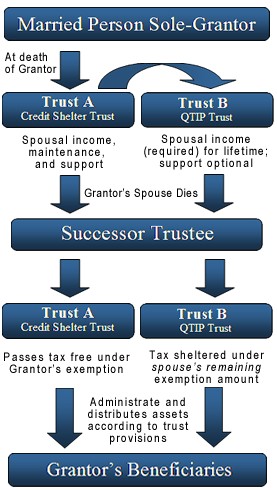

It is a Sole-Grantor Trust designed for a married individual.

|

|

The grantor manages his sole and separate property and any one-half undivided interest in marital (community or tenants-in-common) property in the trust.

|

|

Any estate value exceeding the tax exemption equivalent amount may qualify for the marital deduction (the QTIP portion) and shall be held in-trust for the lifetime benefit of the grantors spouse.

|

|

Neither the QTIP nor the credit shelter portion are under the surviving spouse's control - unless the Grantor permits spousal administration.

|

|

At the death of the surviving spouse, the entire trust estate will be distributed to grantors designated beneficiaries.

|

|

It should be noted that the QTIP portion is in the spouses estate, not the grantors estate, for transfer tax purposes.

|

|

Any of the spouses remaining tax credit can be applied against any transfer tax liability of the grantors QTIP trust estate.

|